Estate Planning Update

Copyright Chip Somodevilla, Getty ImagesWEALTH PLANNING>ESTATE PLANNING

Copyright Chip Somodevilla, Getty ImagesWEALTH PLANNING>ESTATE PLANNING

Could a Change to the Gift and Estate Tax Exclusion Be Retroactive?

A potential shift in the credit amount could lead to unwelcome surprises.

Bob Dietz, Tom Pauloski | Feb 17, 2021

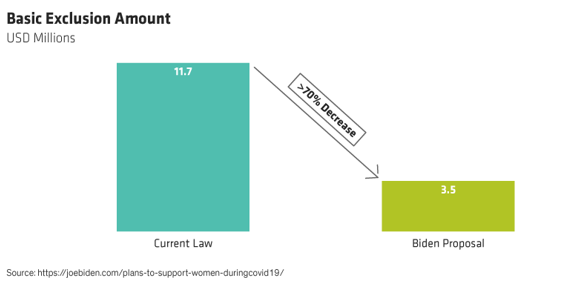

In estate planning circles, there’s much concern about whether Congress may reduce the “basic exclusion amount”—the amount that any person may transfer without imposition of gift or estate tax—and make that reduction retroactive to Jan 1, 2021. Currently, the exclusion is set at an inflation adjusted $11.7 million, but during the 2020 presidential campaign, the Biden camp proposed a reduction of the exclusion to as little as $3.5 million. If that change were enacted by Congress and were made retroactive to the beginning of 2021, individuals who make large gifts early this year may face an unwelcome surprise: A huge tax bill when they file their gift tax returns in April 2022. Although most commentators believe that such a retroactive reduction to the exclusion is unlikely given the current political and economic climate, the possibility can’t be ruled out. But what if Congress were to pass a new law that reduced the exclusion and said nothing about retroactivity? Would gifts prior to the date of enactment be “grandfathered”? Surprisingly, the answer to that question may be “no.”

The Devil You Don’t: IRC Section 2505

Most of the analysis around retroactivity has focused on a potential reduction to the basic exclusion amount, which is defined in the estate tax provisions of the Internal Revenue Code, specifically, IRC Section 2010(c)(3). But the mechanism through which a gift or estate tax is computed is based not on the exclusion, per se, but rather upon a tax credit—the “applicable credit amount”—which is defined separately. For gift tax purposes, the operative provision is IRC Section 2505(a)(1): “In the case of a citizen or resident of the United States, there shall be allowed as a credit against the [gift] tax imposed … for each calendar year an amount equal to … (1) the applicable credit amount in effect under section 2010(c) which would apply if the donor died as of the end of the calendar year,” subject to certain adjustments not applicable to the current discussion.

Read the above-quoted language of Section 2505(a)(1) closely: It provides that the credit against gift tax isn’t the amount of credit under the law that’s in effect at the time of the gift; rather, it’s the credit that would have applied for estate tax purposes had the donor died at “the end of the calendar year [emphasis added].” That credit, in turn, would be based on the basic exclusion amount that’s in effect at year’s end. The ramifications seem significant: If Congress were to enact a law with an effective date on or before Dec. 31, 2021 that reduced the exclusion from $11.7 million to, say, $3.5 million (See chart below), Section 2505(a)(1) may result in a reduced exclusion for a gift made at any time during 2021, even if the new law were silent on retroactivity.

Great … Now What?

Fortunately, several viable strategies may be available to clients who want to avoid retroactive application—by whatever mechanism—of a potential reduction to the basic exclusion amount in 2021. In no particular order:

Disclaimer trust. A disclaimer trust gives the trustee or other recipient of property nine months to decide whether to disclaim a gift if Congress were to reduce the exclusion retroactively. In the event of adverse legislation, the disclaimed gift presumably would revert to the grantor. But there’s a potential conflict of interest: How could a trustee, who owes a duty of absolute loyalty to the trust beneficiaries, refuse a large gift in trust to the benefit of the grantor, to whom the trustee owes no duties whatsoever? This model seems unlikely to pass muster under basic fiduciary principles. If someone other than a trustee (say, a beneficiary) were to disclaim, would that disclaimer be binding on the other beneficiaries of the trust? And if so, would those other beneficiaries have a cause of action against the disclaimant? Each state has its own disclaimer statute, so there’s no consistent answer to these issues.

It may be possible to avoid a conflict by drafting the trust to provide instead for, say, an outright distribution to the grantor’s spouse, which if disclaimed by that spouse, would pass or continue in trust for the benefit of that spouse (under an exception to the general rule that the disclaimant cannot be a beneficiary of the recipient trust) and the grantor’s descendants. There should be no conflict of interest in this case, as the spouse is disclaiming on their own volition, with no underlying fiduciary duties to the beneficiaries of the recipient or continuing trust. In this model, the gift presumably would be disclaimed if Congress didn’t enact adverse legislation. Note that the gift under this model wouldn’t revert to the grantor.

A qualified disclaimer for federal gift tax purposes must comply with the requirements of IRC Section 2518, which include in most cases a written refusal by the disclaimant to accept the property within nine months after the original transfer. Due to this 9-month limit, most estate planning practitioners are waiting to implement disclaimer trusts until at least April 1, 2021, just in case Congress were to enact new tax legislation very late in the year. In addition, the disclaimant can’t have accepted any benefits (for example, dividends or interest) from the disclaimed property. Finally, the disclaimer must be valid under applicable state law; practitioners must ensure that the disclaimer trust is compliant with local standards.

One final word of caution about disclaimer trusts: Sometimes, disclaimants may surprise you! A disclaimant who swears to abide by the grantor’s wishes on April 1st might experience a change of heart nine months later, on New Year’s Eve. And the grantor would have no legal recourse. (April Fools!)

QTIP-able trust. What if a grantor doesn’t want to wait until April or is concerned about whether the designated disclaimant will “do the right thing” when the time comes? One option may be to establish an irrevocable trust that, among other requirements, provides the grantor’s spouse with a mandatory income interest for life. By April 2022, when the grantor’s gift tax return for 2021 is due, the grantor will know whether Congress did or didn’t retroactively reduce the exclusion. If Congress were to make such a change retroactively, the grantor can opt to make a qualified terminable interest property (QTIP) election, in whole or in part, that’s effective as of the date of the gift. In that case, the elected portion should qualify for the unlimited gift tax marital deduction and avoid the imposition of any gift tax. If Congress were to fail to reduce the exclusion in 2021, the grantor could opt not to make the QTIP election. In that case, the gift would use up some or all of the grantor’s $11.7 million exclusion, but again, no gift tax would be imposed.

Importantly, the grantor in this model retains control over whether to make or not make the QTIP election. That is, control over whether a gift is taxable isn’t ceded to a third party, as in the case of a disclaimer trust. Provided that the election doesn’t give the grantor, in effect, a retained power to direct trust property, there should be little risk of a taxable gift or inclusion in the grantor’s estate at death. One way to mitigate that risk would be to administer the trust under identical dispositive provisions, whether the election is or isn’t made.

The caveat? In the case of a QTIP-able trust, the trustee must pay all trust accounting income annually to the beneficiary spouse, which has the potential to send a steady stream of assets back into the taxable estate during that spouse’s lifetime. Those income payments must continue for the beneficiary spouse’s life, even if the grantor and the beneficiary spouse were to divorce, and even if the beneficiary spouse were to remarry after the death of the grantor or after a divorce. It may be possible under the applicable state principal and income act to “control the spigot” of income being paid out to the beneficiary spouse each year by wrapping the trust’s assets in a limited liability company or similar entity, and limiting distributions from that entity, but a QTIP-able trust also must give the beneficiary spouse the power to cause the trustee to make trust property productive of a reasonable amount of income. (Good luck with that under current capital market conditions!) Alternatively, an independent party (for example, a trust protector) may be granted broad powers to amend the trust, presumably including elimination of mandatory income distributions if not necessary to qualify the trust for the unlimited marital deduction.

Defined-value clause. A third option may be a gift that’s subject to a defined-value clause This clause would allow any portion of the gift in excess of the donor’s exclusion, “as finally determined for federal gift tax purposes,” to pass to charity, the grantor’s spouse, a marital deduction trust, or some other recipient without being subject to gift tax.

Such clauses are very common in testamentary estate planning, and frequently are used in connection with sales to irrevocable (intentionally defective) grantor trusts (see below), a popular lifetime wealth transfer strategy. Based upon a line of Tax Court cases that includes Wandry v. Commissioner, T.C. Memo 2012-88; Treasury Regulations Section 25.2511-1(e) (“if the donor’s retained interest is not susceptible of measurement on the basis of generally accepted valuation principles, the gift tax is applicable to the entire value of the property subject to the gift”).and its progeny, a carefully drafted defined-value clause should be given effect, provided that no portion of the gift may revert to the donor.

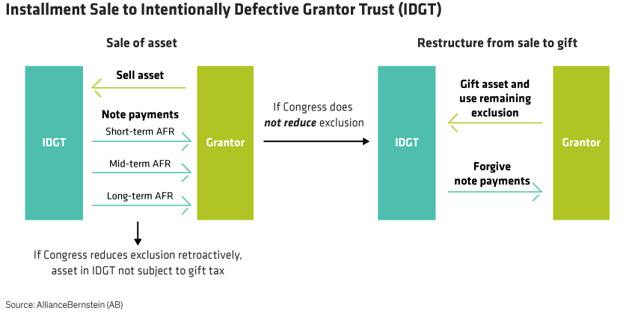

Installment sale or loan in lieu of current gift. The safest option may be to sell,rather than give, assets to an irrevocable (intentionally defective) grantor trust in exchange for a promissory note at the short-, mid- or long-term applicable federal rate (AFR) of interest (see chart below). The benefit? If the exclusion were to be reduced retroactively, assets sold shouldn’t be subject to the gift tax. On the other hand, if Congress ultimately fails to reduce the exclusion in 2021, the grantor can forgive the debt and complete the gift. If the debt is forgiven, in whole or in part, this strategy will use some, or all, of the grantor’s remaining exclusion, and should mitigate the risk of incurring a gift tax.

This option is particularly appealing in the current environment, when interest rates are at or near all-time lows. For example, as of this writing, the short-term AFR, which applies to debt instruments having a fixed term of three years or less, is just 0.12%. If the principal amount of the debt instrument for a current sale or loan were $11.7 million (ignoring, for the moment, whether a modest “seed gift” of a portion of that amount might be used to establish the creditworthiness of the trust), the interest payable from the trust to the grantor would be just $14,040 in the first year. That seems a very small price to pay to avoid a potential gift tax of $3.28 million, if the exclusion amount were reduced to $3.5 million and the gift tax rate were to remain at 40%.

An Unwelcome Surprise

Even if Congress didn’t take a retroactive approach to tax legislation, an unwelcome surprise may still be in store for individuals who make large gifts any time this year. For those considering large gifts, the ramifications of Section 2505(a)(1) are significant, but may, perhaps, be mitigated using one or more of the strategies described herein.

This article was inspired by a Feb. 5, 2021 conversation between Thomas Pauloski and Cynthia Plawker of AllianceBernstein, and Philip Michaels and Nancy Montmarquet of Norton Rose Fulbright US LLP. The authors thank Phil and Nancy for their contributions. Any errors or omissions in this article are the responsibility of the authors alone.